-By Jim Krane*

Over the next few years, Saudi Arabia will complete a 1.2mn b/d expansion of its oil refining capacity (see p8). This allows it to capture a larger portion of the value of its heavy crude, and reduces dependence on the few importers with capacity to handle high-gravity crudes.

But the refining expansion also erodes the kingdom’s “swing supplier” role in global energy markets. Saudi Arabia will be less willing or able to vary its oil production to suit market needs, because it will find itself diverting a larger share of crude oil into the domestic market, leaving it with a smaller portion earmarked for export.

For the kingdom, the shift toward refining is a logical one. It represents the typical path of a country moving away from low-technology commodity exports to a higher level of national development. Refining also supports industrial development, domestic employment, and more advanced integration into the global economy.

But there is a hitch. Saudi Arabia’s hard security needs depend on America, under the old “oil for security” relationship. These ties, in turn, hinge on the kingdom remaining a major oil exporter. To avoid undermining this relationship, the Saudis are cautiously augmenting it with a more diverse set of economic and investment ties with individual companies and countries, including China.

SWING SUPPLY ROLE RELIQUISHED?

In November, Saudi Arabia demonstrated a willingness to deviate from its typical behavior. It refused to let market demand dictate its level of oil production, since doing so would mean relinquishing market share to higher-cost non-Opec competitors. Opec left production quotas unchanged in its 27 November meeting, and oil prices fell dramatically, losing about half of their June values by December. As Baker Institute research showed, the swing supply role has since been taken up, in part, by US shale producers.1

Saudi Aramco’s refining push will exacerbate this trend by presenting a new and steady source of demand that is less sensitive to prices. The kingdom may not only refuse to cut output at times of low prices, but, since a greater level of its production is earmarked for the domestic economy, Aramco may be less able to increase production in response to outages and market shocks.

Saudi Aramco’S Worldwide Refining Ventures

Saudi Aramco’S Worldwide Refining Ventures

| Saudi Aramco’s worldwide refining ventures | |||

| Refinery name and location | Completion | Shareholders | Capacity (b/d) |

| Domestic | |||

| Jeddah | 1967 | Saudi Aramco | 100,000 |

| Yanbu | 1979 | Saudi Aramco | 240,000 |

| Riyadh | 1981 | Saudi Aramco | 124,000 |

| Yanbu (Samref) | 1983 | Saudi Aramco (50%), ExxonMobil | 400,000 |

| Jubail (Sasref) | 1986 | Saudi Aramco (50%), Shell | 305,000 |

| Ras Tanura | 1986 | Saudi Aramco | 550,000 |

| Petro Rabigh | 1990 | Saudi Aramco (37.5%), Sumitomo Chemical | 425,000 |

| Jubail (Satorp) | 2014 | Saudi Aramco (62.5%), Total | 400,000 |

| Yanbu (Yasref) | 2014 | Saudi Aramco | 400,000 |

| Jazan* | 2018 | Saudi Aramco | 400,000 |

| Total domestic capacity (by 2018) | 3,344,000 | ||

| International | |||

| China: Fujian Refining and Petrochemical Company | 2007 | Saudi Aramco(25%), Sinopec, ExxonMobil | 240,000 |

| USA: Motiva Enterprises | 2002 | Saudi Aramco (50%), Shell | 1,070,000 |

| Japan: Showa Shell Oil | 2004 | Saudi Aramco (15%), Shell | 395,000 |

| South Korea: S-Oil | 1991 | Saudi Aramco(35%), S-Oil | 669,000 |

| Total international ventures | 2,374,000 | ||

| Overall total refining capacity | 5,718,000 | ||

| Source: Saudi Aramco 2013 Annual Report; *under construction. | |||

GROWTH OF SAUDI REFINING

Saudi Aramco and its joint venture partners are in the final stages of a nearly 60% expansion of domestic refining capacity from 2.1mn b/d in 2013 to 3.3mn b/d by 2018. Globally, Saudi Aramco will own a share of refineries with combined total capacity of 5.7mn b/d (see table).

Three new refineries in the kingdom will produce a slate of sophisticated products calibrated to stringent European standards. Output will be dominated by ultra-low sulfur diesel (about two-thirds of output) and high-quality gasoline (about a quarter of output). The remainder includes heavy distillates, petrochemical inputs like benzene and propylene, as well as residual sulfur and petroleum coke.

The first of the three is the Satorp refinery in Jubail, a joint venture with France’s Total, which began operations in 2014. Satorp has since reached full processing capacity of 400,000 b/d of Arabian Heavy crude (MEES, 20 March).

Across the Arabian Peninsula at Yanbu on the Red Sea, another 400,000 b/d heavy crude refinery has also reached initial start-up. The Yasref refinery, Aramco’s second joint venture with China’s Sinopec, made its first shipment of high-quality diesel fuel on 15 January.

At the southern end of the Red Sea, a third 400,000 b/d refinery is under construction at Jazan, wholly owned by Saudi Aramco. The Jazan refinery is scheduled for start-up in 2018 (MEES, 27 February).

Investment rationale for these refineries dates to the run-up in crude prices in the mid-2000s. At the time, many analysts claimed that high prices stemmed from insufficient crude oil for market demand. Saudi officials responded that the shortage was not in crude oil, per se, but rather in refining capacity for the full spectrum of oil, including heavy and sour crudes. Aramco embarked on a refining expansion that would capitalize on lower prices and reduced demand for heavy crude.

The refining push was also designed to meet rising demand for transportation fuel inside the kingdom. Saudi Arabia has been a net importer of gasoline for most of the last decade. Jodi data show it imported about a quarter of its gasoline and a fifth of its diesel in 2013.

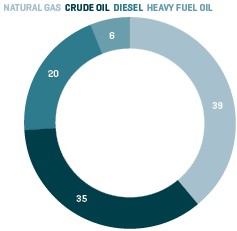

At the same time, Saudi Aramco sought to reduce the ever-larger amounts of crude oil burned in domestic electricity generation. Some 60% of Saudi Arabia’s 278 terawatt-hours of electricity production in 2013 came from liquid fuels – more than half of which was unrefined crude oil – with the remaining 40% from natural gas (see figure 1).

It was hoped that refining would reduce the domestic “crude burn” by separating out valuable light and middle distillates, including gasoline, diesel and jet fuel. The lighter products could be distributed domestically or exported, while the remainder – low-value heavy fuel oil – could replace crude in electricity production. Crude could thus be “stretched” and the opportunity cost of diverting crude oil into the power sector would be reduced.

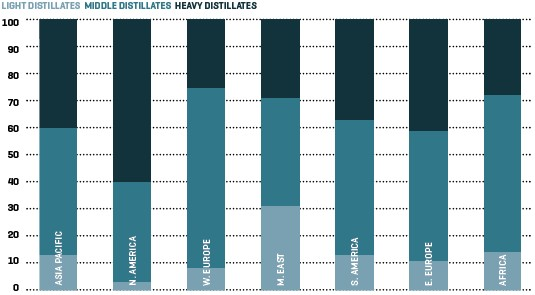

However, as Saudi Aramco sought to attract joint-venture partners, the company found it had to adopt a refining slate that maximized production of high-value products in demand in Europe, Japan and North America. This meant installing cracking and coking units to extract more light and middle distillates from heavy crude, while nearly eliminating residual fuel oil output. Unlike the Middle East, these markets have very little demand for heavy distillates (see figure 2).2

While this strategy has succeeded in soaking up demand for heavy crude, it fails to provide much low-value residual feedstock for power generation. The result is that the kingdom will become an importer of heavy distillates by 2020 while burning valuable, domestically refined diesel that could otherwise be exported. In 2013 the Saudi Electricity Company consumed about 200,000 b/d of diesel, fueling about a fifth of its power output.3

DOMESTIC CRUDE OIL DEMAND

Boosting refinery capacity comes at the price of adding yet another source to the accumulating pull of domestic demand for Saudi crude oil, which has grown by an average of 6% per year for the past decade. In 2013, domestic consumption, including refinery intake – some of which is exported in the form of products – reached 3.1mn b/d, roughly 27% of total oil production. At that rate of growth, all else constant, domestic oil consumption would double by 2025.

Saudi demand for crude is exacerbated by fast growth in the power generation sector, where low, subsidized electricity prices have encouraged consumption and waste. Peak crude burning that has reached 800,000 b/d could top 1mn b/d by 2020, as the kingdom continues to build oil-fired power plants. Outside the Middle East, oil-based power generation has been largely replaced by much cheaper coal, natural gas and nuclear power.

Intensifying domestic crude burning coupled with a 1.4mn b/d increase in crude shipments to Aramco refineries inside and outside the kingdom signal that Saudi Arabia is moving beyond its long-held role as the world’s market-balancing supplier of crude oil. Recent data show slipping Saudi crude exports, alongside flat or rising production. Assuming that Saudi crude production remains constant at around 10mn b/d, the amount of crude available for export could fall below 5mn b/d by 2020.4

Reductions in crude exports would be partly balanced by increased exports (and reduced imports) of refined products, as the kingdom transitions away from imported fuel and becomes a long-term net exporter of diesel and a shorter-term net exporter of gasoline and heavy fuel oil.

These trends, outlined in the table, point to a shift in export dynamics of the Gulf. As the Saudis move beyond crude, neighboring Iraq may continue to increase exports, perhaps capturing markets that Saudi Arabia can no longer serve.

Of course, subsidy reforms under discussion in the kingdom could greatly reduce consumption. For instance, rationalized gasoline prices could reduce long-run demand by about a fifth.5

FIGURE 1: SAUDI POWER GENERATION BY FUEL, 2013 (%)

FIGURE 2: REGIONAL CONSUMPTION OF REFINED PRODUCTS BY DISTILLATE

Source: Jadwa Investment.

GEOPOLITICAL IMPACT

Saudi Aramco’s refining expansion is yet another sign of Saudi Arabia moving away from its long-held role as a simple supplier of crude oil to the world. The kingdom will have less flexibility to “swing” with fluctuations in price and demand, not least because joint venture refining partners espouse profit-maximizing goals that may exclude reductions in output.

These changes will affect Saudi Arabia’s geopolitical role. Spare capacity, and the willingness to deploy it in tandem with US intervention in the Middle East, has made Saudi Arabia a valuable foreign policy partner with Washington and helped protect the oil-importing world from volatile prices.

As Saudi Arabia’s geo-economic profile changes, one must ask how the kingdom can maintain the strategic backing of the United States under the longstanding “oil for security” arrangement. By one estimate, America spends $50bn a year to protect the Gulf monarchies from external threats in exchange for maintaining reliable flows of oil to markets. Can the Saudis move beyond crude exports while keeping America’s protection?

The refining expansion lays the groundwork for an alternate multilateral security arrangement. Rather than relying solely on Washington, the kingdom’s refining ties integrate it with powerful importing countries which, in turn, become stakeholders in Saudi Arabia’s stability and security.

This strategy involves deepening ties with the United States, but also with other big importers, including those where Saudi Aramco owns equity in refining businesses. In America, Saudi Aramco owns a 50% share (alongside 50% held by Shell) in the three Motiva Enterprises refineries in Texas and Louisiana.

Aramco supplies a dominant and discounted share of the more than 1mn b/d of crude oil which Motiva refines into gasoline and diesel. Most of the output is sold under the Shell brand at some 8,200 service stations across America. In this way, Motiva guarantees Saudi Arabia a prominent role in US energy security, whether or not the kingdom maintains its traditional market-balancing role. Saudi Arabia’s global refining and petrochemical ventures are also tethering the kingdom more directly to Japan, South Korea and China, now the world number one oil importer.

However, Saudi Aramco’s experience in the United States presents a cautionary tale. Aramco originally intended to leverage its Motiva refineries to become the number one supplier of imported oil to the United States.

But the Saudi plan was undermined by an unexpected cascade of new oil production in the United States and Canada. By 2004, Canadian exports surpassed the share from the kingdom. Saudi Aramco was forced to deepen discounts to maintain market share. By 2014 Canada supplied America with two and a half times more crude than Saudi Arabia (MEES, 13 March). Nevertheless, Motiva allowed the Saudis to retain a major presence in the US market.

The costs of this strategy are mounting. The delivered price of Saudi crude into the United States is already Riyadh’s lowest worldwide, despite comparatively high freight costs. Wood Mackenzie’s Alan Gelder calculates that Saudi Aramco suffers a $3 to $6 opportunity loss for each barrel it markets in America rather than Asia, its best market. “That is the value the Saudis put on their relationship with the USA,” Gelder says.

In short, Riyadh wants to preserve US strategic interest – even as the kingdom jettisons its swing supply role – by using discounts to guarantee a long-term American home for its oil.

CONCLUSION

Saudi Arabia is reshaping itself as a big supplier and consumer of complex, high-value refined petroleum products, rather than a simple exporter of raw material. This transition is made more difficult by the kingdom’s need to retain the US security umbrella. Saudi Arabia is compensating by ensuring it retains a large share of US crude imports and refined gasoline sales, while also developing similar integration with Japan, China and Korea.

*Jim Krane is the Wallace S. Wilson

Fellow for Energy Studies at Rice University’s Baker Institute for Public Policy, in Houston. This piece

is based on the key findings of an article published in the Q1 2015 issue of Energy Policy.

http://bakerinstitute.org/research/saudi-arabia-moves-beyond-crude-oil/

{{{{SAUDI ARABIA AND CANADA COMPETING FOR THE US IMPORT MARKET. }}}}}

SOURCE: EIA.

1Jim Krane and Mark Agerton, “Effects of Low Oil Prices on U.S. Shale Production: OPEC Calls the Tuneand Shale Swings.” Baker Institute Research Paper. February 2014.

http://bakerinstitute.org/media/files/files/7cd5c58c/CES-pub-OPEC-021315.pdf

2 Alan Gelder, Global Practice Lead for Refining and Marketing, Wood Mackenzie. Author interview, Dec.19, 2014.

3Jadwa Investment. “Outlook for Crude Oil Refining: Focus on the Saudi Refining Sector in a GlobalContext.” Research note. November 2014.

4“Saudi Direct Crude Burn Plan Can Only Work Short-Term, Says FGE.” MEES Vol. 57 No. 17, Apr. 25, 2014.

5Ibid, MEES, Apr. 25 2014. Estimates are from FGE.

6Not including NGLs. See: “New Gulf Refineries to Make Middle East Major Products Exporter.” MEES Vol. 57 No. 31, Aug. 1, 2014.

7 If gasoline prices were raised from $0.57 to $2 per gallon, a non-linear price elasticity calculation finds that long-run demand would shrink by about 21%, when price elasticity is estimated at 0.2. This assumes that consumers are relatively insensitive to price.