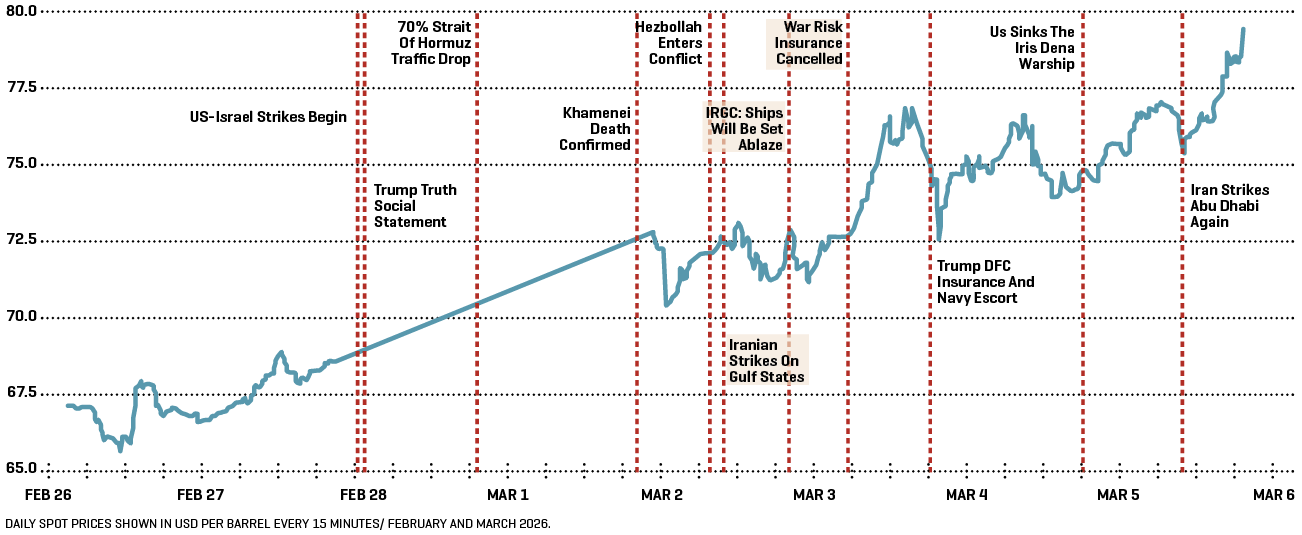

When markets opened Monday following the US – Israeli strikes on Iran and the escalation of conflict across the region, crude prices reacted immediately. Brent moved higher as traders priced in geopolitical risk around the Strait of Hormuz, the corridor through which roughly one-fifth of global oil supply and a significant share of LNG exports transit each day.

Yet the reaction was initially measured given the scale of the shock. Prices rose modestly at the start of the week, with Brent surging sharply at the open and briefly moving above $82/B before settling near $77-78/B on Monday, as concerns grew over potential disruption to shipping and regional energy infrastructure. As attacks on Gulf energy infrastructure intensified and tanker traffic through the Strait of Hormuz fell dramatically, with many vessels delaying or diverting transit, prices rose further, with Brent moving into the mid-$80s before entering the $90 range by Friday.

The most notable feature, however, was not the magnitude of the price move, but the market’s ability to absorb a rapid sequence of geopolitical developments without translating them into a sustained supply shock. Several energy infrastructure sites were targeted during the week, yet oil prices moved only modestly and stayed within the same trading range.

Understanding why requires examining how the structure of energy markets has changed. Today’s oil market processes geopolitical shocks through a multi-layered system of inventory buffers, logistics signals, data transparency, and algorithmic trading, reducing uncertainty compared with earlier crises.

Part of the explanation lies in how modern oil markets process risk. Geopolitical headlines still trigger immediate price responses, often amplified by algorithmic and momentum-based trading strategies that react quickly to new information. But those initial signals are rapidly tested against observable indicators of physical supply: inventories, tanker movements, freight rates, spare capacity, and refinery demand. In this sense, the market is making a distinction between geopolitical escalation, physical supply disruption and alternative global supplies.

INVENTORIES AS SHOCK ABSORBERS

At the time the conflict began, global oil fundamentals were relatively comfortable. Commercial inventories across OECD economies remained close to historical averages, and demand growth had moderated compared with the post-pandemic surge. Market sentiment was also influenced by a dominant narrative of oversupply—despite ongoing debate about whether the market was truly in a glut.

Equally important, several major consuming countries have built significant strategic buffers. China in particular has accumulated substantial crude inventories in recent years. Total Chinese crude stocks are estimated at 1.1–1.3bn barrels, including both strategic and commercial storage. Some estimates place China’s total reserve holdings at around 900mn barrels, equivalent to roughly two to three months of imports. These inventories have expanded as China has maintained import levels that frequently exceed immediate refining demand, allowing the country to build stocks when market conditions are favorable. In 2025, the gap between crude supply and refinery runs averaged about 1.13mn barrels per day, peaking at 2.67mn b/d in December, contributing to further inventory accumulation. This stockpiling provides short-term insulation against supply disruptions, especially for a country that sources a large share of its imports from the region.

These buffers give the market flexibility that was largely absent during earlier oil shocks. Unlike the oil shocks of the 1970s, when commercial inventories were much smaller and large government strategic reserves had not yet been established, today’s markets have greater buffer capacity against sudden supply disruptions. Today, the presence of commercial stocks and strategic reserves allows temporary disruptions to be absorbed without immediate shortages. As a result, even amid escalating tensions in this major energy producing region, markets could assess the risk against available buffers rather than reacting to fears of an immediate supply collapse.

In that sense, inventories function as the oil market’s first line of defense, allowing the system to absorb short-term shocks while traders assess whether disruptions will persist.

DATA, ALGORITHMS, AND THE SPEED OF PRICE ADJUSTMENT

Another reason the market reaction remained contained lies in the availability of market data and the speed at which modern oil markets process it. During earlier oil crises—most notably the 1973 Arab oil embargo and the 1979 Iranian revolution—price discovery often unfolded over months rather than hours. Oil prices quadrupled between late 1973 and early 1974, rising from roughly $3/B to nearly $12/B. Prices also surged following the Iranian revolution, even though the physical supply loss was relatively limited.

In fact, that disruption removed only about 4–6% of global oil supply, yet uncertainty and panic amplified the price increase over time. At the time, traders had limited visibility into global inventories, shipping flows, and spare capacity, allowing geopolitical fears to dominate price formation.

Today the information environment is very different. Markets continuously track inventories, tanker movements, refinery runs, freight rates, and insurance costs. This data allows traders to assess supply conditions in near real time.

Algorithmic trading systems process these signals almost immediately. Freight costs, futures spreads, shipping activity, and refinery margins are incorporated into pricing models within minutes to hours, allowing markets to recalibrate quickly as new information emerges.

The reaction to this week’s geopolitical events indicates that the market was effectively evaluating whether the situation represented a headline shock or a genuine disruption to physical flows—and if so, how long such disruption might last and whether alternative supplies could compensate. That visibility matters. Data availability and transparency now function as a stabilizing element of energy security, allowing traders to assess supply buffers and physical flows in near real time.

In that sense, data transparency and algorithmic trading together helped prevent the kind of panic-driven volatility that characterized earlier oil crises.

SPARE CAPACITY STRANDED AT HORMUZ

While production capacity remained intact, the first signs of disruption appeared not in oil fields but in the logistics system surrounding the Strait of Hormuz. As tensions escalated, marine insurers cancelled or sharply repriced war-risk coverage for vessels operating in the corridor. Without insurance, most commercial tankers cannot operate, prompting shipowners to delay departures or anchor outside the Strait. Shipping data showed vessels waiting while freight rates and insurance premiums surged.

This occurred even as Opec+ moved forward with plans to unwind some of is previous voluntary production cuts, agreed at a pre-scheduled meeting on 28 February. Yet spare capacity only stabilizes markets if oil can physically reach consumers. When shipping becomes constrained, available production capacity does not translate into deliverable supply.

In effect, the corridor tightened before any enforceable closure of the Strait itself. The constraint emerged not from damaged infrastructure or halted production, but from the growing reluctance of insurers and shipowners to operate in a high-risk environment.

For markets, the implication is clear: spare capacity existed, but it was temporarily stranded. The Strait did not need to be formally closed by Iran for flows to slow; logistical risk alone was sufficient to restrict the movement of oil through one of the world’s most critical energy corridors. In practice, Hormuz does not need to close to disrupt markets; it only needs to become too risky to use.

LNG MARKETS REACTED MORE SHARPLY

When Qatar suspended LNG exports and declared force majeure on LNG shipments and supplies, global gas prices reacted far more aggressively than oil prices.

The explanation lies in the structural characteristics of the LNG market. Global liquefaction capacity operates with limited spare margin, and cargoes are often tied to long-term contracts. When a major supplier such as Qatar—responsible for roughly 20% of global LNG exports—interrupts shipments, replacement volumes are difficult to mobilize quickly.

As a result, LNG markets are far more sensitive to disruptions in a single exporting country than oil markets, which benefit from deeper storage and greater supply diversification.

This structural difference explains why gas prices surged even as crude markets remained relatively contained.

DURATION REMAINS THE KEY VARIABLE

Despite the relatively contained price response, risks remain significant. The current market reaction reflects an implicit assumption that disruptions will be temporary. Inventories and spare capacity can cushion short interruptions to supply flows.

However, the calculus changes if the conflict becomes prolonged.

Early signs of logistical strain have already appeared. With tanker movements disrupted through the Strait of Hormuz, Iraq has been forced to reduce production as storage capacity filled and shipments could not move. If disruptions persist, similar constraints could emerge for other producers whose export routes depend on transit through the Strait. The duration of the disruption is therefore critical.

Over time, extended disruptions would gradually erode inventory buffers, tighten shipping capacity, and increase insurance costs. A prolonged conflict would not only deepen logistical bottlenecks but could also expose regional energy infrastructure—including export terminals, pipelines, and loading facilities—to greater risk. The impact would not remain confined to crude markets. LNG supply chains, electricity generation, petrochemicals, and industrial production would all begin to feel the pressure.

For major consuming economies—particularly China, which relies heavily on oil and LNG imports from Hormuz—sustained disruptions could raise energy costs across multiple sectors, including power generation and petrochemical manufacturing.

In that scenario, the effects would extend well beyond oil prices. What begins as a logistical disruption in a single chokepoint could evolve into a broader energy and economic shock, especially if physical infrastructure is damaged or export capacity in the region is impaired.

WHAT MODERN OIL MARKETS CAN - AND CANNOT - ABSORB

The recent regional geopolitical tensions, reveals how the structure of oil markets has changed. Larger inventories cushion shocks. Data transparency and algorithmic trading help limit panic-driven price movements by improving the market’s ability to assess uncertainty. Together, they help prevent the prolonged panic that defined earlier oil crises.

For now, those mechanisms are working. Prices have risen, but the market response has remained measured as traders distinguish between geopolitical escalation and actual disruptions to supply.

But resilience has limits.

Inventories can absorb short interruptions. Markets can process information faster than ever. Yet neither can fully offset a prolonged disruption to shipping, infrastructure, or regional energy flows. For now, the market is pricing a manageable disruption. Whether that assessment holds will depend on a single factor: how long the disruption lasts.

Crude Oil Exchange Prices With Iranian Conflict Event Indicators

*Dr Sara Vakhshouri is Founder and President of SVB Energy International; Founding Chair, IWP Center for Energy Security and Diplomacy; Adjunct Professor, Georgetown University School of Foreign Service, and Senior Fellow at Oxford Institute for Energy Studies (OIES).