By – Sarah Emerson*

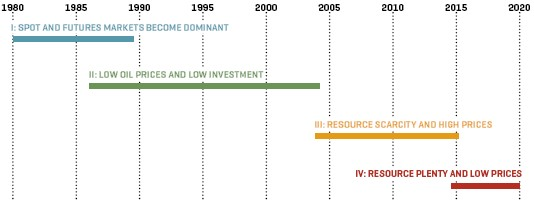

The history of global oil markets can be characterized by a division into four key phases:

1) The emergence of market forces...which led to...

2) Low prices and low investment… which led to...

3) High prices and resource scarcity… which recently gave way to...

4) Low prices and resource plenty.

We may now be on the verge of a fifth period which threatens to take the form of a turn away from the transparent, efficient, deregulated global oil market of the last 35 years.

THE 1980S TURN TO MARKETS

The liberalization of global oil markets got underway in the 1980s, the decade after the second oil crisis. In the US, oil prices were decontrolled; vehicle fuel economy standards were introduced in the 1975 Energy Policy and Conservation Act; and natural gas and nuclear power gradually replaced oil in power generation.

Meanwhile, higher world oil prices stimulated non-Opec production and cut global oil demand. In the market for the marginal barrel of crude (the spot market), prices fell below Opec’s elevated and fixed price. Not surprisingly, independent refiners, traders and even the integrated majors bought more crude on the spot market.

By the early 1980s, crude oil transactions at spot prices or prices tied to the spot market accounted for more than 50% of total international crude trade.

Within Opec, the role of swing producer in defense of higher prices became increasingly untenable for Saudi Arabia. Ultimately, the Saudis abandoned this role, a market share war ensued and prices collapsed in 1986 (MEES, 31 March 1986). Since then, almost all of the world’s oil has been sold bilaterally with transactions linked to market-based pricing, such as netbacks or formulas tied to spot or futures prices.

‘Market forces’ became the dominant organizing principle of the global oil sector.

Multilateral lending shaped by the market-friendly Washington Consensus encouraged the deregulation of domestic oil industries and the liberalization of petroleum product pricing all over the world as countries opted to integrate into the large, transparent and, for many years, low-priced global oil market.

The view that market forces, rather than government policies, were best suited to allocate resources equitably was mirrored by the rise of Reagan-Thatcher laissez-faire conservatism of the 1980s and the eventual collapse of the Soviet bloc by the early 1990s. The devaluation of the Russian ruble and the Asian financial crisis later in the 1990s were seen as further evidence of the folly of policies that ran counter to market forces in global capital markets. In the early 2000s, the market-friendly approach of the George W Bush Administration, China’s accession to the World Trade Organization (WTO) and further deregulation of financial markets continued to underscore the dominance of the ‘market.’

A HISTORY OF GLOBAL OIL MARKETS IN FOUR PHASES

THE PERCEPTION OF RESOURCE SCARCITY

In a system dominated by the cost-reducing pressure of market forces and the proliferation of oil suppliers, it is not surprising that oil demand grew far more than oil investment during the last two decades of the 20th century. This led to the elimination of spare capacity throughout the supply chain, making the oil sector vulnerable to disruptions and accidents, which encouraged higher prices in the early years of the 21st century.

In a market of lean capacity and with an emerging consumer like China, the financial markets saw oil (as well as other commodities) as clear targets for investment. The interest of institutional investors in buying and holding commodities and the exploitation of lax leverage requirements by investment banks is well known and contributed to the ‘super cycle’ in commodity prices. Some of the same behaviors in other markets contributed to the financial crisis in 2008, which in turn exacerbated the great recession.

THE REALITY OF RESOURCE PLENTY

Not long after the financial crisis, the promise of US shale came into view (MEES, 2 August 2013). The combination of fracking and horizontal drilling lifted the US oil producing sector. US shale and Canadian oil sands swelled North American oil (and natural gas) supplies, redrawing the oil trade map as North American oil imports were pushed away, and headed to Asia.

With the Chinese economy soaring, Asian countries became the overwhelming market for key Middle East producers. This trade expanded OPEC revenues considerably, which peaked at $1.2 trillion in 2012, double 2009 levels (MEES, 10 February).

The North American supply boom had shifted global markets back to plenty. The decades of resource scarcity and high prices came to an end. In a move reminiscent of the 1980s, Opec responded with a market share war that contributed to the surplus and brought oil prices down to 1990s levels (MEES, 19 December 2014).

Even with Opec cutting output in a landmark agreement at the end of 2016, it will not be enough to bring back the age of scarcity. Rather, the global oil markets look headed for tenuous balance, vulnerable as much to new supplies as new disruptions.

A TURN AWAY FROM TRADE

Looking back over the last 35 years, market forces and transparent pricing have shaped supply and demand all over the world, in spite of (and sometimes helped by) Opec’s periodic distortion of price signals. One result has been tremendous geographic expansion in international oil trade, which has made petroleum the model of a highly functional global market. The 2015 lifting of the US ban on crude oil exports may go down in history as the capstone of the era of global oil trade (MEES, 23 December 2016).

As we sit here in 2017, two developments threaten that model.

One is currently embodied by the Trump Administration whose ‘America First’ policies are likely to push the United States closer to energy autarchy. It is too early to know for sure, but references to Republican tax reform hint at policies that will penalize corporations with foreign supply chains through border adjustments or import fees. Oil and gas will not be immune to these policies.

Moreover, the United States will not be alone in this. The United States’ willingness to impose trade barriers will be met by the same. The strength and efficiency of global oil trade may allow for a nimble response at first, but the trend will be towards less free trade and thus less efficiency in supply, demand and price.

The other threat is China’s actions in the South China Sea. In 2016, China’s crude imports reached more than 7.0mn b/d, approximately 70% of domestic refinery demand with Saudi Arabia, Iran, Iraq, Kuwait and Oman all shipping record volumes although this was not enough to stop Russia grabbing number 1 spot (see chart). It is not surprising that China has tremendous interest in the offshore oil reserves of the South China Sea. Reserves estimates vary but China’s Ministry of Land and Resources estimates 55-130bn barrels of oil reserves and 700 tcf of natural gas.

Obviously, the security and development of the energy resources of the South China Sea are critical to China’s effort to reduce its dependence on imported energy.

Another concern is the security of sea lanes through the South China Sea and Straits of Malacca. Crude oil from the Arab Gulf and Africa, which comprises 50% of China’s imports, transits the Malacca Strait and passes through the South China Sea to reach Southern China. After processing in Chinese refineries, petroleum products such as gasoline, gasoil, and jet fuel are exported to Southeast Asian and African countries on the same route back.

In addition, large quantities of liquefied natural gas (LNG) from Qatar and Australia move through the South China Sea to China. As a result, China sees the energy transit routes in the South China Sea as critical to its national security.

The buildup of China’s military assets in the Spratly and Paracel Islands, and its naval force at Hainan Island, has been striking and portends military standoff at best and conflict at worst in this critical trade corridor.

This physical threat to trade could parallel or even respond to the regulatory threat to trade under consideration in the US. Efforts to ‘control’ certain trade flows by each of these countries will not only inhibit trade, but invite retaliation. Both would be steps backward for the global oil market.

China’s Top Crude Suppliers (‘000 B/D)

China’s Top Crude Suppliers (‘000 B/D)

TRADE DISRUPTIONS WOULD MEAN HIGHER PRICES

In a 25-year outlook, one cannot put too much weight on current trends, but clearly the next decade will be marked by oil trade-related developments that will be a departure from the past. Any disruption to easy trade will create pockets of supply/demand imbalance and impact price relationships between trading hubs. New price relationships will reorganize trade.

If current trade flows are relatively efficient, reorganization will likely increase costs and thus add to oil prices. Some consumers will live with higher oil prices while others live with lower prices. There should be a similar impact on the profitability of oil operations all over the world, making investment even more speculative, and thus more costly.

In sum, a turn away from trade is likely to make oil more expensive.

*Sarah Emerson is President of Energy Security Analysis, Inc. and Managing Principal of ESAI Energy, LLC (www.esaienergy.com). [email protected]