Lebanon’s hopes of joining the much-hyped East Med gas club have suffered another setback. After a decade of delays and political crises, 2020 looked to finally be the year that Lebanon stumbled its way to the starting blocks. However, plans to start offshore drilling and launch a second licensing round have both been pushed back.

Racked by socio-economic upheaval, Beirut is still hopeful that a Total-led consortium (Total 40%op, Eni 40%, Novatek 20%) will drill two wells this year, while the second offshore licensing round is still expected to close and see contract awards by year’s end.

But the specter of delays, both political and technical, is once again haunting Lebanon’s gas ambitions and further delays remain a real possibility. On 13 January, (since replaced) Energy Minister Nada Boustany announced that the second offshore bid round – set to close 31 January – had been pushed back three months to 30 April.

On its own, the delay isn’t the end of the world. An updated timeline from the Lebanese Petroleum Administration (LPA) suggests the negotiating period will be expedited and the council of ministers will award acreage in July. But the reasons behind the delay are more worrying.

“The direct reason for the delay is political,” says Mona Sukkarieh, a political risk consultant and co-founder of Middle East Strategic Perspectives. “At the time, there were many doubts that a government could be formed soon enough, so it was better to be cautious given that the bids are only valid for a few months. But I believe there were some doubts over companies’ willingness to bid as well, despite considerable expressions of interest.”

Investor concerns are understandable, with mass protests recently ousting the last government after just nine months on the job (MEES, 1 November 2019). While a new government was formed this week, the announcement was met with further protests. Worryingly, the increasingly heavy-handed response of security forces means that protests are turning increasingly violent. On top of that, the country is fending off a banking-debt-currency crisis (MEES, 20 December 2019), with March default looking likely.

A source at the LPA argues that whilst the political crisis contributed to the delay, the decision was equally motivated by several interested firms asking the LPA to delay the bid round. Chinese state firm CNOOC asked for a two-month extension to analyze the data, whilst Total, Eni and Novatek asked for an additional three months – presumably to take Block 4 drilling results into account. The LPA has also held discussions with Qatar Petroleum, BP, Wintershall Dea, Shell, and a Russian firm, but hadn’t received any bids ahead of the 31 January deadline.

NEW CABINET

The newly formed government – constructed from several political parties (including Iran-backed Hezbollah) calling itself a “technocratic” cabinet –should (at least temporarily) provide for a (slightly) more positive outlook. Whether the new cabinet will manage to secure parliament’s approval is another obstacle – particularly as several parties (including former Prime Minister Saad al-Hariri’s party, the Future Movement) refused to participate.

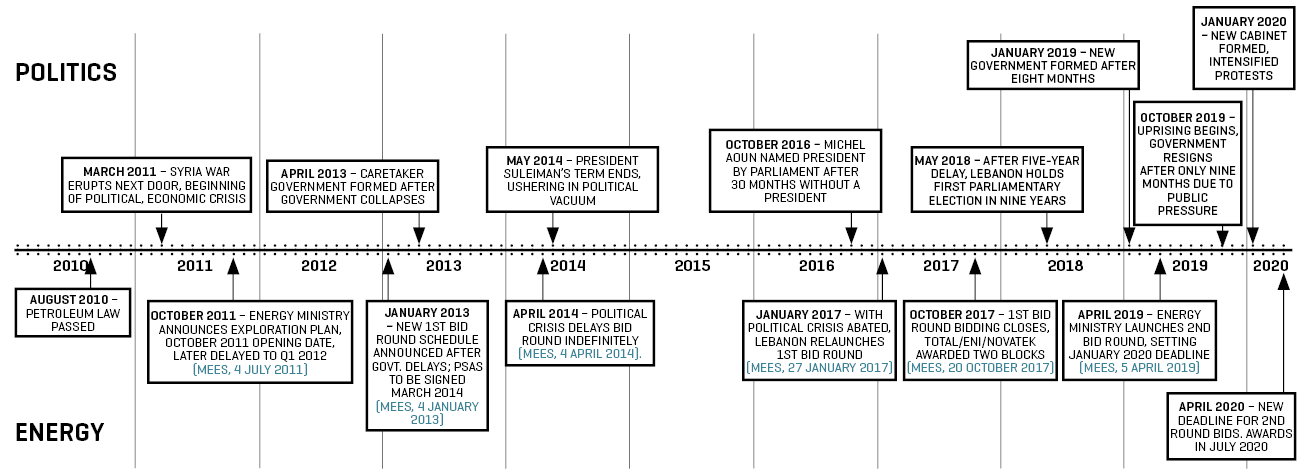

The formation of a new cabinet at least means Lebanon is less likely to suffer another extended political vacuum, the likes of which have had devastating consequences in recent years. Dysfunctional politics was a key reason why the country’s inaugural bid round-launched to considerable IOC fanfare in 2013 (MEES, 17 May 2013) – didn’t see contracts awarded until late 2017 (see timeline).

To attract investment, Lebanon needs to avoid a political black hole. This is especially the case given the current market situation where oversupply has forced prices down and a slew of new LNG projects points towards continued low prices. In this environment exploration in a frontier territory with political instability is far from an attractive prospect.

DRILLING DELAY

If the Total-led consortium manages to strike viable volumes of gas in its upcoming drilling campaign, the results (or lack thereof) of second bid round results will suddenly seem a lot less important. But for results, anxious onlookers will have to wait. A company source working on Lebanon’s first offshore well, the Byblos-1 in Block 4, tells MEES that the contracted drillship has an issue with the blowout preventer and riser, and will miss its January drilling target.

The source expects “at least” a month’s delay and possibly longer, which whilst not a major blow, will further push back the 55-day drilling campaign and potentially Lebanon’s second well in Block 9 that the drillship is scheduled to drill in September or October (MEES, 20 December 2019). In between the two Lebanese wells, the ‘Tungsten Explorer’ is contracted to drill multiple wells for Eni in Cyprus – including Block 8 where Turkey is currently threatening to drill a well (MEES, 24 January).

Total contracted Vantage Drilling’s ‘Tungsten Explorer’ drillship, aiming to begin operations in December or January (MEES, 30 August 2019). But Marine Traffic data shows the drillship still moored offshore Egypt where it’s been drilling Eni’s Nigma-1 prospect in the Northeast Ha’py Block (MEES, 13 December 2019).

LEBANON: A DECADE OF DELAYS AND DISORDER