US shale growth is proving resilient. Though output growth will slow with lower oil prices, it will rebound rapidly at any sign of a sustained pricing upturn – putting a cap on the extent to which prices are likely to rise, likely for several years.

- By Professor Paul Stevens*

Since June 2014, the international price of crude oil has fallen by around 60%. Since the start of this year, Brent has averaged around $54/B. Given that the average price between 2008 and 2013 was $99/B (2013 dollars), this can be viewed as a “low” price. The key question is how long the price is likely to stay low?

Saudi Arabia’s strategy behind the decision by Opec on 27 November not to cut production was that lower prices would reverse the market weakness that generated the price collapse (see p14). This is by increasing demand and reducing supply growth, especially in United States’ tight oil production. So the answer to the question “how long will prices take to recover?” depends upon the responsiveness of supply and demand to the fall in price.

The belief in Opec was that the weak oil demand seen in 2014 was the result of a generally poor global growth performance. Certainly this was part of the story. But part of the explanation of the disappointing performance was also demand destruction following the inexorable rise in prices since 2004. This was reinforced when India and China, both strongly driving global oil demand growth in the last ten years, introduced domestic oil price reform significantly reducing the subsidies, which had done much to encourage growing oil consumption. By definition, even if global economic performance does improve this year, some of the lost oil demand will not return. This will be strengthened as consumer governments see an opportunity to increase sales taxes on oil products meaning lower crude prices will not translate into lower product prices.

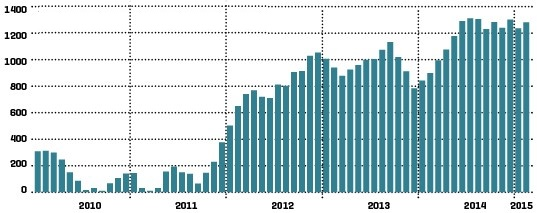

‘BREAK-EVEN’ VS ‘SHUT-IN’ PRICESS

As for supply, Opec appears to have failed to grasp the fundamental change to the economics of oil production created by the shale technology revolution in the United States. Central to this is the difference between “break-even prices” and “shut-in prices”. “Break-even prices” are the fully built-up cost of production including the required return on capital and will determine whether there will be investment in new producing capacity. This is therefore relevant for production into the future. How far into the future depends upon the lead-time on upstream projects. This varies enormously but for conventional oil can be between five to ten years. “Shut-in prices” are the variable costs and will determine whether existing production, which may be running at a loss, actually closes down. This is relevant for what will happen to current production in the near term. There is a wide spectrum of estimates for both prices. Break-even prices have been put at $60-90/B and shut-in prices somewhere below $40/B. However, as lower prices slow upstream activities, these prices, emerging from a five-year frantic tight oil boom in the US, fall dramatically as costs fall. Thus supply may be slower to respond that many have assumed.

NO CLEAR SLOWDOWN... YET: US CRUDE OUTPUT Y-O-Y GROWTH* (‘000 B/D)

*3-MONTH MOVING AVERAGE. SOURCE EIA, MEES CALCULATIONS.

SHALE WELL ‘FRACKLOG’ PUTS CEILING ON PRICES

There is a further complication which will seriously delay any significant price recovery. Before June 2014, and as part of the tight oil frenzy in the US, a large number of tight oil wells were drilled but not completed. Thus while the horizontal lateral has been drilled, they have not been subject to hydraulic fracturing and are therefore not producing. The reason for this is simply because current oil prices make completion economically unattractive. This is being referred to as a “fracklog of wells”. Estimates vary but it has been suggested that it applies to some 3,000 wells. Assuming a production of 800 to 1,100 b/d per well, this represents a potential production level of between 2.4mn and 3.3mn b/d. This puts a ceiling on the price of oil for the foreseeable future. If oil prices rise, at some point they will reach a level that encourages well completion. As soon as this price is reached, new supply will come on-stream very quickly - within a matter of months. This will choke off any price recovery. This cap on prices will remain in force until the “fracklog” is cleared and the lower investment, as a result of low prices, begins to affect new capacity from conventional fields. This process is likely to involve years rather than months.

Of course any price forecast of this sort requires a health warning. Since June, oil prices appear to have lost any semblance of any geopolitical premium as the over-supply has dominated. There is always the possibility of some political event in the Middle East scaring the proverbial horses. As always, there is currently a depressingly long list of potential candidates ranging from an Israeli attack on Iran in response to any deal over Iran’s nuclear program to an escalation of Saudi involvement in Yemen (see p16). However, absent the return of a geopolitical premium, the “low prices” seen since June of last year will be around for some time.