By- Ali Aissaoui*

For all their differences, OPEC countries share the same uncertain outlook: they can hardly insulate their economies from the vagaries of international oil markets. Yet almost all seem to be trying to defy the current oil price collapse by pursuing to varying degrees counter-cyclical economic policies. This is particularly the case of core OPEC countries including Saudi Arabia, the dominant oil player and strong advocate for the policy of defending OPEC’s market share, even if that comes at the expense of oil prices – the policy which won out at OPEC’s November meeting (MEES, 28 November 2014).

In this context, Saudi Arabia’s high reliance on petroleum for export earnings and budget revenues has brought the sustainability of its external and fiscal positions under the spotlight. The external position is straightforward to assess given the country’s healthy net foreign assets of over 33 months of import cover. As far as the fiscal position is concerned, the situation is more complicated. The question is not so much whether Saudi Arabia can sustain low oil prices, as it most definitely can. Rather, the question is: how much of a buffer has been built and how long could it last? Although such a buffer should be understood as combining both fiscal surplus and borrowing capacity, we restrict ourselves to the former in order to keep the question as focused as possible.

UP TO $750BN BUFFER

The Saudi budget for 2015, which is a little higher than that for 2014, projects total expenditure of $229.3bn and revenue of $190.7bn (MEES, 2 January). The resulting apparent deficit of $38.6bn represents some 5% of 2015 GDP. Neither the revenue breakdown nor the oil price assumptions underpinning these figures are available. However, what matters here is the expenditure side of the budget, from which we derive a fiscal break-even oil price and thus the time it takes to deplete the country’s fiscal buffer for different oil market price assumptions. Before that, however, we must identify the location and size of this buffer.

Saudi Arabia has neither a dedicated sovereign wealth fund (SWF) nor a fiscal stabilization fund (FSF). Instead, the government has trusted its financial surpluses to SAMA. Therefore, in addition to the assets the central bank controls to inter alia meet balance of payments financing needs, it also acts as an asset manager for the Saudi treasury. Accordingly, at the end of 2014, SAMA’s net foreign assets totaled $724.3bn and its liabilities in the form of government deposits were $416.2bn. While the latter aggregate is the most relevant for fiscal operations, it is also the narrowest gauge of the state’s fiscal buffer. We have estimated that other autonomous government institutions, including pension funds (PPA and GOSI) and the Public Investment Fund, hold together some $335bn of assets that could potentially strengthen the fiscal buffer. Therefore, we estimate the broader fiscal buffer to be at least $751.2bn.

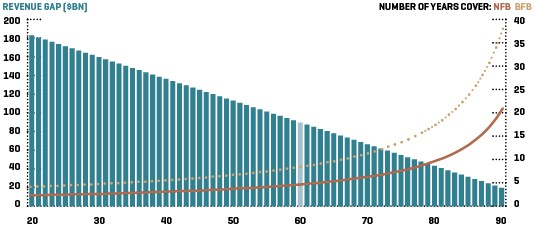

SAUDI ARABIA: YEARS OF FISCAL BUFFER AT VARIOUS OIL PRICES ($/B, OPEC BASKET)

SOURCE: APICORP RESEARCH.

HOW MANY YEARS’ COVER?

The calculation of the number of years future deficits could be covered by the fiscal buffer range of $416.2bn to $751.2bn can be approached as the relative difference between the fiscal break-even oil price and the oil market price. The former is a virtual price that balances the budget. This increasingly prevalent concept is as simple to define as it is complex to estimate. As demonstrated in previous articles**, it is a function of total budget expenditure; petroleum production, exports, royalties and taxes; non-oil tax revenues; and production costs. These parameters combine to generate a median fiscal break-even oil price of $98.50/B. Therefore, assuming 2015 budget expenditure and an OPEC basket price of $60/B – that is to say current market expectations for 2015 – the number of years’ budget deficit cover is found to be between 4.6 for the narrow fiscal buffer (NFB) and 8.4 years for the broader fiscal buffer (BFB) (see graph).

By definition and construction, the number of years of budget deficit cover is a rational (nonlinear) function of the oil market price whose asymptote is the fiscal break-even oil price. To avoid reaching that asymptote we have restricted the oil price variable (the X-axis) to a maximum price of $90/B. As already indicated, the revenue gap can be bridged comfortably under current oil market expectations. More significantly, in the worst-case scenario where oil prices collapse further to $20/B (a case envisioned by the Saudi oil minister – MEES, 2 January), the length of the cover is between 2.3 and 4.2 years.

Our findings suggest that, all other things being equal, Saudi Arabia can largely afford current fiscal expenditure; in the worst-case scenario for up to four years. When adding other strings to the budget bow, including a large untapped borrowing capacity, the country’s fiscal power appears almost inexhaustible. This means that this dominant oil player has indeed the means of its current policy. However, the longer oil prices remain depressed, the more depleted the fiscal buffer will be and the more likely it is that efforts to maintain fiscal sustainability will become extremely complicated.

*Ali Aissaoui is Senior Consultant at APICORP. This article is published concurrently in APICORP’s Economic Commentary dated March 2015. The views expressed are those of the author only. Comments and feedback may be sent to [email protected]

** See for instance “Modeling OPEC Fiscal Break-Even Oil Prices: New Findings and Policy Insights” (MEES, 26 July 2013).