Despite geopolitical interpretations of Saudi oil policy, the reality is more prosaic.

-By John Sfakianakis*

The passing of King Abdullah and the advent of King Salman is a time of continuity in the Kingdom’s oil policy not a time of radical change. Saudi Arabia took a bet in the most recent OPEC meeting in November in deciding whether or not to cut oil output. The parlor game of divining why Saudi Arabia has decided not to cut production and instead allow the price of crude to go into free fall has spawned a raft of wild guesses and conjectures.

The kingdom no doubt has made a bold bet that it can maintain its output without jeopardizing either the stability of the oil market or its own long-term economic well-being.

Such a risky move can be made only by a country that has finances as strong as Saudi Arabia’s. Its motives are also supply-oriented as a lot of non-OPEC oil was gaining market share.

Had it not discounted oil prices, ‘free riders’ such as Russia, Venezuela, Iran and Nigeria would have benefited and undercut Saudi crude in the process. Saudi Arabian Oil Minister Ali Naimi articulated the kingdom’s policy in an interview with MEES on 21 December and made clear that Riyadh would stick to its guns even if prices fell to $20/B, a signal that drove prices even lower.

$734BN CUSHION

However, few anticipated that oil prices would slump in such a short period of time. No producers outside OPEC have so far indicated a willingness to cut their output. Hence, the burden would again have fallen on Saudi Arabia. Crude oil no doubt is the kingdom’s long term revenue lifeline but Riyadh has built up enough of a cushion to sustain a lower price environment in the medium term. Today, the country sits on $734 billion in foreign assets, nearly the size of its entire economy. Moreover, it has one of the world’s lowest debt to GDP ratios. Even with oil at $50/B, Saudi Arabia can withstand high spending. In addition, most of the mega projects it is undertaking are funded by surpluses from previous budgets.

The country’s elite technocrats are aware that the kingdom could sustain current plans for a few years even if spending remains high and oil prices remain low. However, intergenerational equity issues and the gradual depletion of reserves would doubtless be in the minds of these technocrats. Certainly spending it all in a short period of time would not be wise. The bet, however, is predicated on a pick-up in economic activity throughout the emerging and developed world.

DÉJÀ VU? NOT THIS TIME

Saudi Arabia’s oil policy makers do not believe there is a déjà vu in world oil prices similar to the slump in 2009, when Brent crude hit a low of $33/B. But they do believe that oil prices, partly due to speculators, have been excessive on the downside - just as they were on the upside back in 2007 when oil prices hit an intraday high of $147/B. Such overshooting occurs often in commodity markets, especially oil. Back then it was high demand for crude oil from China and India, whereas today it’s the opposite. There is exaggerated concern about a slowdown in China, other Emerging Markets in general as well as Europe and also over anemic growth in Japan. Markets often overreact on both sides of the pendulum, so consensus views dominate, and one-way bets, this time on the downside, are made. The global economy is nowhere close to the global financial crisis witnessed in 2008-2009. We believe that Emerging Markets will recover more dynamically in the years to come and so will oil prices.

Calculations about geopolitics and shale were perceived as the key to understanding Saudi Arabia’s petroleum policy. Many have interpreted Saudi Arabia’s real intentions as containing Iran’s ambitions in the region. However, although Iran has been hurting ever since oil dropped below $145/B, the country’s history shows that the price of crude doesn’t make it less aggressive and expansive over time. Oil was falling for most of the 1980s when Iran was battling Iraq while its oil revenues dropped by 75%.

It would also be too simplistic to think that Saudi Arabia was behind the collapse of the Soviet Union due to it single handedly bringing down oil prices. It’s equally simplistic to imagine that Russia will alter its policy toward Syria just because oil prices have plummeted. An attempt to undermine the US shale industry by dropping prices is a policy that might have short term benefits, but technology has a tendency to improve over time. Saudis know all too well that in the 1980s the North Sea oil industry survived quite well even as oil prices slumped.

Rather than driving the US shale industry out of business, as some have speculated, Saudi Arabia would be better off buying out most of the industry, especially at today’s bargain prices. For all the fanfare in the US about its oil independence, severe doubts remain about shale’s long term sustainability as well as the ability to manage its environmental damage.

Many have argued that the days when Saudi Arabia was the linchpin of the oil market are over, but, like it or not, the reality is that the kingdom remains the producer of last resort. What ultimately explains Saudi behavior is a lot more prosaic than we have been led to believe: the Saudis are still haunted by the painful experience of the 1980s when they cut production, only to see oil prices plummet from $35 to below $10. They’ve made it clear they are not about to go down that path.

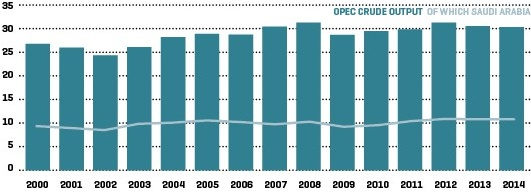

SAUDI ARABIA HOLDS CRUDE OUTPUT STEADY (MN B/D)

SOURCE: MEES ESTIMATES.

*John Sfakianakis is Middle East Director at Ashmore Group.