By-Ali Aissaoui*

Will OPEC continue to play a pivotal role in world oil markets? I shall try to approach the topic from an energy and investment policy perspective along three lines. Firstly, I shall take a brief look back at OPEC’s role and achievements. Secondly, I will tentatively explore what the future holds for the organization and what implications that could have on its investment strategy. I will conclude by hopefully giving a satisfactory answer to the topic’s central question.

LOOKING BACK BEFORE LOOKING AHEAD

Despite the evolving role of OPEC, its twin fundamental interests remain fairness and stability. Fairness is about the equitable distribution of the global oil surplus in providing a reasonable return to investors and ensuring that neither producers nor consumers claim a disproportionate share of the economic rent captured through oil-related taxes and revenues. But while fairness is in the eyes of the beholders, stability is a more general concern. The fact that today OPEC contributes 42% of global oil output while its oil proved reserves represent 72% of the world’s total, delineates the role of “residual supplier” that the organization has been reduced to and the implied responsibility for market stability.

This crucial role is derived from the view that global oil demand is first met by supply from non-OPEC producers, then by OPEC. Within this framework, Saudi Arabia, which currently accounts for 22% of OPEC oil reserves and for 31% of its output, holds the bulk of OPEC (and the world’s) spare capacity. This has given it a de facto leadership role that includes acting as a swing producer. In the first half of the 1980s for instance, in a context of major structural changes that dramatically shrank the demand for OPEC oil, Saudi Arabia shouldered almost alone the burden of stabilizing oil prices, before precipitating their collapse to regain market share. Since then, responsibility for output modulation has fallen on an increasing number of members.

OPEC’s mixed attempts at navigating market swings and cycles have brought it closer to the top of a steep learning curve. In recent years, the organization has greatly improved its efficacy. Recent examples of this include the period 2003-07, when OPEC output was collectively boosted to meet rapidly increasing global demand with the aim of containing soaring prices. Conversely, in the second half of 2008, OPEC implemented swiftly deep production cuts to contain a sudden and unexpected collapse of oil prices. Also since 2009, OPEC has been rather effective in signaling to the market its fair/preferred prices, which, as we shall later have the opportunity to note, have tended to coincide with its weighted average fiscal break-even price. This is not to mention advertising its members’ upstream investments.

Yet, OPEC’s influence on prices through output modulation, price signaling, or investment streams could have been more effective. In any case, it could be hardly said that OPEC has stabilized what matters most to its members. To be sure, OPEC real rent per capita has dramatically improved in recent years reaching $2,320 in 2013, after having lingered at less than $1,000 over two decades or so between 1985 and 2005. Though some would argue that today’s real rent per capita is only a little more than half the level achieved at the turn of the 1970s, discounting the context of the 1979 Iranian revolution.

THE FUTURE FOR OPEC?

Looking ahead, OPEC will continue to face long-term structural changes and uncertainties in both its external and domestic landscape. On the one hand, the profound shifts in global energy demand and energy supply patterns we have seen in recent years are likely to deepen. Surely, we will continue to witness further effects of the energy security-climate change nexus on petroleum markets. On the demand side, efficiency progress in vehicles and alternative transport fuels will likely continue reducing the importance of oil. On the supply side, current challenges from the potential impact of light tight oil (LTO) and other unconventional oil sources will become more compelling should the ‘US Shale Revolution’ spread successfully to other parts of the world. Looking further ahead, one wonders what other ‘energy revolutions’ lie in store at the confluence of technology and innovation, politics and policy, and the economics of viability of frontier oil development?

On the other hand, in the domestic market, OPEC members are heading down an unsustainable energy consumption path causing huge opportunity costs from lost export revenues. Policy makers’ responses to rapidly rising energy demand (resulting from profligate consumption patterns) have tended to focus more on the prospect of supplying alternative energies and less on managing demand. While energy efficiency pronouncements have yet to materialize, energy pricing and subsidy reforms remain a real policy and political conundrum. In these circumstances, our projections indicate that export share of oil production is likely to shrink further from the current 60%, to just 40% by 2040.

In the medium term, as LTO, oil sands, and offshore pre-salt oil surge, OPEC will face diminishing market share and difficult internal dynamics. The latter stems from the fact that Iraq, Iran and Venezuela are major potential sources of capacity and output growth. Normalization of Iran’s relations with the West and a return to stability in Iraq would lead to production gains that could challenge Saudi Arabia’s leadership. Furthermore, growing exports of oil products risk eroding the demand for crude oil in some importing countries. In this respect, Saudi Arabia, which has recently invested heavily in export-oriented refineries, may now be perceived more as a “refiner” whose influence on crude oil prices is diminishing. Indeed a shift from trading crude to trading products risks rendering quotas on crude production meaningless as a tool to govern oil exports and prices. To maintain its leadership, Saudi Arabia may need to keep and wield more crude oil spare capacity.

In the longer term, most central scenarios expect OPEC to regain its market share, as demand in Asia – and especially in China and, increasingly, in India – grows, while non-OPEC supply starts running out of steam. The US Energy Information Administration (EIA) for instance anticipates in its new International Energy Outlook (IEO, September 2014) that, in a Reference case where oil prices rise moderately, OPEC’s market share would increase from a low of 39% in 2020 to a little more than 42% in 2040. This involves core OPEC countries contributing additional output of 15.6mn b/d between 2013 and 2040 compared to a non-OPEC output increment of 13.1mn b/d. The OPEC contribution, which is expected to increase by a modest, though challenging, 2.2mn b/d during the remaining part of the present decade, would rise significantly thereafter to 5.7mn b/d in the 2020s and 7.7mn b/d in the 2030s.

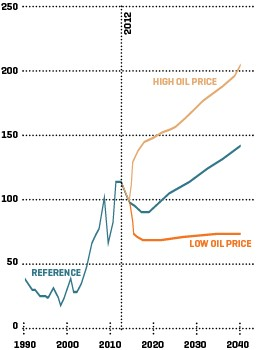

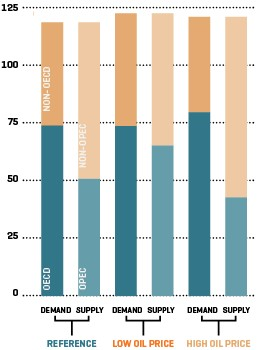

But is OPEC willing to invest if the oil price at which global supply and demand balance is widely uncertain? Among other factors, price trends influence consumption and production, which in turn drive price changes. To assess the range of potential interactions between supply, demand and prices, the 2014 IEO considers three price cases: the Reference (central) case where prices trend towards $141/B in 2040 (in 2012 dollars), and two alternative cases: a Low Oil Price and a High Oil Price cases where prices hit $75/B and $204/B, respectively by 2040. These three cases illustrate some, but not all, of the range of uncertainties in the future of the oil market. Accordingly, the corresponding call on OPEC oil is expected to vary in a wide range: from 43.7mn b/d in the High Oil Price case to 65.3mn b/d in the Low Oil Price Case (see graphs). Therefore a major challenge for OPEC and its members as they develop their investment strategy will be finding a trade-off between pre-commitment and flexibility before the uncertainty is resolved.

Should OPEC be willing, is it able to invest? Our perceptual mapping of the energy investment climate, which combines three attributes (potential investment, country risk and the enabling environment for the development of the oil industry), suggests a poor overall score for more than half of the OPEC countries, among which are those previously identified as having the biggest potential for growth. In addition, the latter countries will hardly be able to finance their share of upstream investment so long as their fiscal break-even costs are above the OPEC weighted average, which currently stands, according to our estimates, at $105/B.

WILL OPEC CONTINUE TO PLAY A PIVOTAL ROLE?

In conclusion, and to answer our central question, one could say that future uncertainties will continue to hamper OPEC’s decision-making and policies. Despite these uncertainties, however, OPEC should take a coordinated long-term view of investment and production with the objective of maximizing the net present value of oil rent accruing to its members. Normally, the higher the price the more incentive there is to invest; but high prices may entail lower call on OPEC oil, leading in turn to lower prices. While the resulting cycles are likely to revive old dilemmas (and dramas), they will not prevent OPEC from continuing to play a pivotal role. However, that role could be undermined if policymakers fail to address new challenges, including: rationalizing domestic energy consumption and prices to maintain export potential; improving the investment climate and creating a more enabling environment for the oil industry; moving towards sustainable, non-oil-rent-dependent alternative sources of funding; and, within the internal context of OPEC, agreeing on new rules of leadership and collective action to ensure more effectiveness.

*Ali Aissaoui is Senior Consultant at APICORP. This article is based on a presentation made at the IIF 2014 MENA Regional Economic Forum (Manama, 29-30 September). The views expressed are those of the author only. Comments and feedback may be sent to: [email protected]

THE EIA’S LATEST INTERNATIONAL ENERGY OUTLOOK:

BRENT OIL PRICE SCENARIOS (2012 US$)

APICORP RESEARCH - REPRODUCED FROM EIA’S IEO 2014.

CALL ON OPEC UNDER EACH SCENARIO (mn b/d).

APICORP RESEARCH - REPRODUCED FROM EIA’S IEO 2014.